Yuh Review: The Swiss All-in-One Finance App

Let’s be honest: Swiss banking is famous for being solid, but it’s also known for its high fees and sometimes confusing complexity.

Enter Yuh. Launched in 2021, it promises to change the rules. Yuh is a 100% digital “all-in-one” financial app designed to be your single stop for paying, saving, investing, and even your pension.

But does it live up to the hype? In this Yuh Review, we take a deep dive to find out.

Can I Trust Yuh?

This is the most important question. When it comes to your money, you need to know it’s safe.

Yuh itself isn’t a bank; it is fully owned by Swissquote. The banking services are provided by Swissquote, which is a fully-fledged bank authorized by FINMA (the Swiss financial regulator).

So, what does that mean for you? Your cash deposits are protected up to 100’000 CHF by the Swiss deposit protection scheme. This is the exact same protection you get at any traditional Swiss bank.

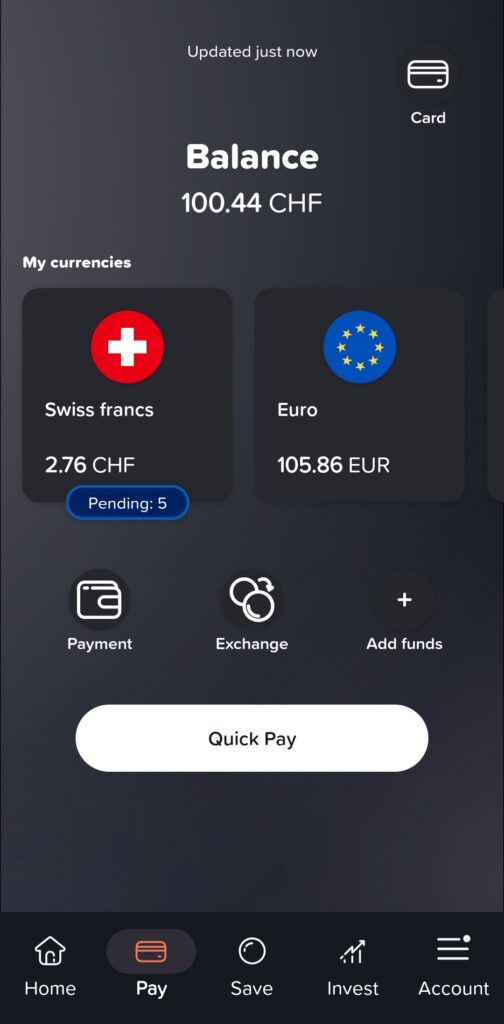

The “Pay” Function: Your Everyday Account

This is where Yuh replaces your traditional bank account. The main draw is that the account is genuinely free. Here’s what you get:

- A completely free account with zero monthly management fees.

- Your own Swiss IBAN.

- A free Debit Mastercard (physical or virtual) which includes “Yuh Pocket,” a free purchase insurance (check their site for the full coverage details).

- Full support for Swiss essentials: Yuh fully supports both TWINT and eBill, making your daily transactions simple.

- A built-in multi-currency account that lets you hold 13 different currencies (like EUR, USD, GBP, etc.) all in one place.

- A flat 0.95% exchange fee when you exchange money between these “pockets” or pay for something in a currency you don’t hold.

- A nice bonus: The card comes with “Yuh Pocket,” a free purchase insurance for items you buy with it (check their site for the full coverage details).

Now, let’s look at the costs for specific actions.

- Sending Money:

- In Switzerland (and Liechtenstein): Free for all 13 currencies Yuh supports.

- Abroad (SEPA): Free if you send EUR. It costs 4 CHF if you send other currencies.

- Getting Cash:

- In Switzerland: You get one free withdrawal per week from any ATM.

- Abroad: Be careful here, as it costs 4.90 CHF per withdrawal.

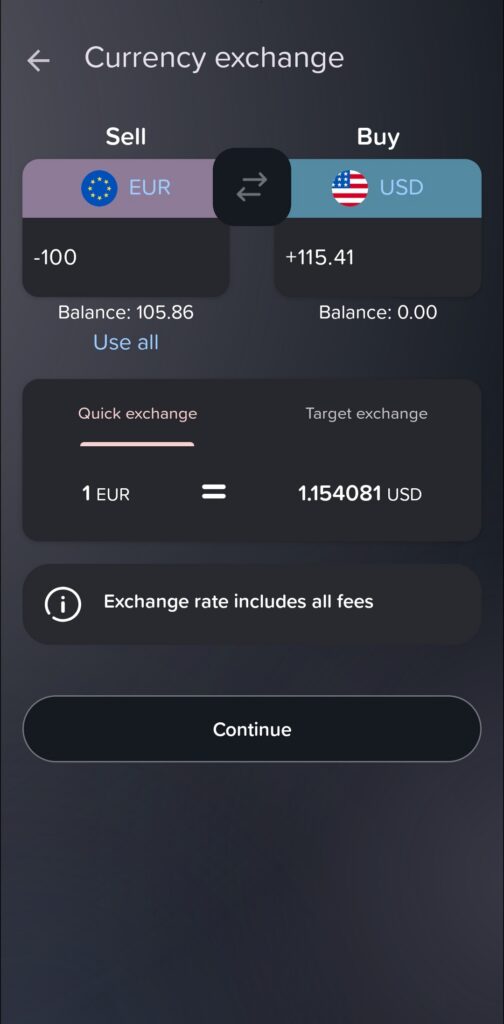

- Currency Exchange:

- When you exchange money between your currency “pockets” or pay for something in a currency you don’t hold, Yuh charges a flat 0.95% exchange fee.

- While this is transparent, it’s important to note that this is significantly more expensive than specialized travel apps like Revolut or Wise, which offer lower fees.

The “Invest” and “Pillar 3a” Functions: Building Wealth

This is where Yuh gets really interesting, combining banking with wealth building.

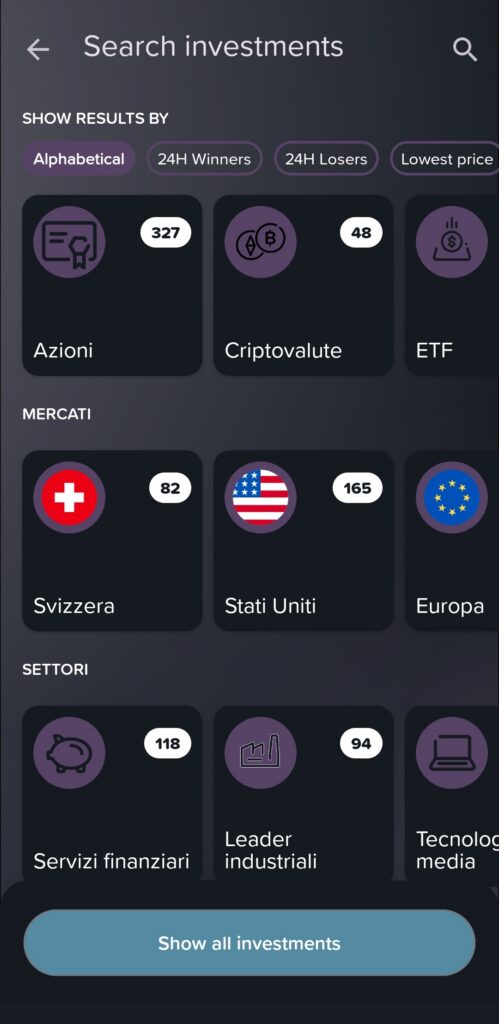

Easy Investing

Yuh makes investing incredibly accessible. It offers a wide range of assets: stocks, ETFs (exchange-traded funds), bonds, and even cryptocurrencies.

The minimum investment for any trade is just 10 CHF, a feature made possible by fractional shares.

Fractional shares allow you to buy a small “slice” of even the most expensive stocks. This means you can own a piece of a high-value company by investing just 10 CHF, instead of needing thousands to buy a full share. The result? You can build a diversified portfolio from day one, even with a small budget.

It’s crucial to understand how the crypto feature works. Yuh is not a crypto wallet. You can buy and sell crypto within the app, but you cannot deposit crypto from an external wallet or withdraw your crypto to a private wallet. You can only sell your holdings back to Yuh for cash.

Investment fees are very straightforward:

- Trading (buy/sell stocks, ETFs): 0.5%

- Crypto (buy/sell): 1.0%

- Custody (holding your assets): 100% free.

The Savings Plan

You can set up automatic, recurring investments to build your portfolio over time.

KEY BENEFIT: For recurring investments into a selection of ETFs, Yuh charges 0 commissions on the purchase (you still pay the 0.5% on a sale). This is a huge plus for long-term automated saving.

Pillar 3a

Yuh also offers a Pillar 3a solution, which is essential for tax-advantaged retirement saving in Switzerland.

It’s an investment-based 3a. You open a single 3a account right in the app. Inside that account, you can choose from 5 different investment strategies. These are defined by their equity (stock) percentage—from 20% to 99%. The remainder is invested in a mix of bonds, real estate, commodities, and cash. (You can see a detailed breakdown of each strategy here).

Flexibility is a major plus. There’s no minimum opening amount. You can set up weekly or monthly automatic deposits, or just add single payments whenever you like, starting from just 10 CHF.

The fees are very competitive: a flat 0.50% annual fee on your invested assets.

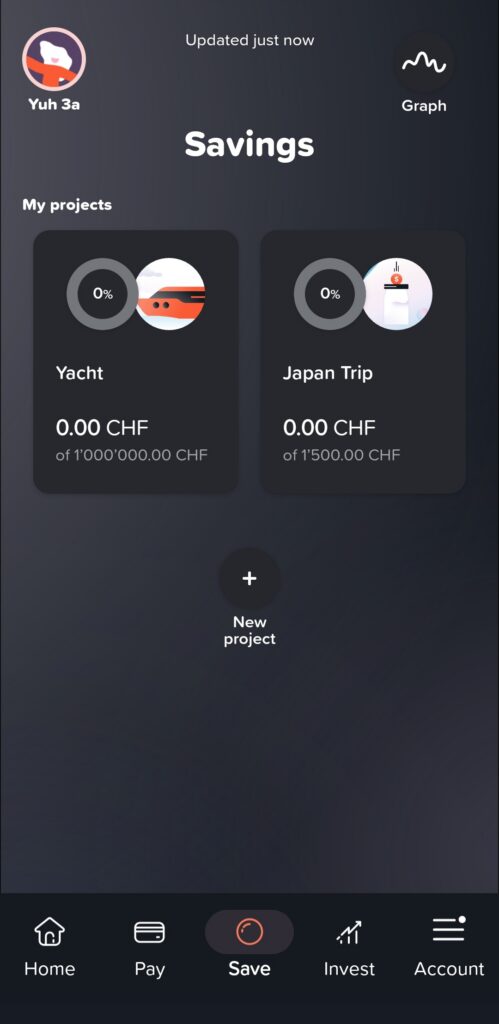

The “Save” Function: Your Digital Piggy Bank

Yuh also has a dedicated “Save” function, which allows you to create “Savings Projects”.

Think of this as a digital envelope system for your goals (like “Vacation” or “New Laptop”). You can create a project, set a goal amount, and fund it either with manual transfers or automatic, recurring deposits.

This is a great psychological tool for separating your savings from your daily spending money. However, it’s crucial to understand that this is purely an organizational tool, not an investment. The interest rate on funds held in these Savings Projects is 0%.

A Bonus for Families: The “Yuh 14+” Teen Account

Yuh also offers a dedicated, free bank account for teenagers aged 14 and up. It’s designed to give teens financial independence safely, and it’s a very strong offering for families.

The teen account includes its own Debit Mastercard and access to TWINT.

Crucially, the Yuh 14+ account has a massive advantage over the standard adult account: there are no currency exchange fees and free cash withdrawals worldwide. This makes it an exceptional card for teens, especially for travel, language stays, or online purchases in other currencies.

The account also has no overdraft risk, so teens can’t spend more than they have.

The Bonus: What is “Swissqoin”?

You’ll see “Swissqoin” (SWQ) mentioned a lot. What is it?

Think of it as Yuh’s loyalty program. It’s a special crypto token (like a digital rewards point) that Yuh gives out as a bonus.

How do you get it?

- Welcome Bonus: You can get a starting bonus of 250 SWQ by making a single initial deposit of at least 500 CHF.

- Referrals: Get 250 SWQ for inviting friends who also make a single initial deposit of 500 CHF.

- Trading: Get 5 SWQ every time you make an investment.

- Paying: Get 1 SWQ for card payments.

You can sell your Swissqoins for cash or transfer them to other Yuh users. It’s a fun bonus, but it’s not the main reason to choose the app.

Analysis: Pros and Cons of Yuh

Let’s break it down. No app is perfect.

Pros

- Truly “All-in-One”: It’s the simplest app in Switzerland that genuinely combines everyday payments, TWINT, eBill, investing, and Pillar 3a.

- Genuinely Free Account: You pay zero monthly management fees for your main account, which is a huge win.

- Ideal for New Investors: The 10 CHF minimum, low 0.5% trading fee, and 0-commission ETF savings plans make it incredibly easy to start.

- Simple & Cheap 3a: The 0.50% fee is excellent, and the total flexibility on deposits (starting from 10 CHF) is perfect for those who don’t want to commit to large annual payments.

- Excellent Teen Account: The free “Yuh 14+” account is a standout feature for families, offering 0% currency exchange fees and free cash withdrawals worldwide.

- Strong Everyday Features: You get useful perks like one free cash withdrawal per week in Switzerland, a built-in 13-currency account, and free purchase insurance (“Yuh Pocket”).

- Maximum Reliability: It’s backed by Swissquote and has the 100,000 CHF Swiss deposit guarantee.

Cons

- No Direct Cash Deposits: As a 100% digital app, Yuh has no physical branches or partner locations to accept cash. If you need to deposit cash, you must first deposit it into a traditional bank account and then transfer it to your Yuh IBAN.

- High Costs Abroad (for Adults): The 0.95% currency exchange fee and 4.90 CHF for cash withdrawals are significantly more expensive than specialized competitors like Revolut or Wise.

- Crypto is a “Walled Garden”: You cannot deposit or withdraw crypto to an external wallet. It’s a “closed system,” not a true crypto wallet.

- High Crypto Fees: At 1.0%, the fee for buying crypto is higher than on specialized exchanges.

- Pillar 3a Limits: You can only open one 3a account. This is a drawback for advanced tax planning, as competitors like VIAC allow 5 separate “pots” to optimize tax on withdrawal.

- Zero Interest on Savings: Yuh offers “Savings Projects,” but the interest rate on them is 0%.

For full transparency, all fees are listed clearly on their official pricing page.

The Verdict: Who is Yuh For?

So, what’s the final word?

Yuh is an excellent choice for…

- The “Digital Daily” User: Anyone who simply needs a modern, reliable, and free primary account. The combination of a free Mastercard, Swiss IBAN, TWINT, and eBill covers all essential daily banking needs in Switzerland, with zero monthly fees.

- The “Passive Saver & Beginner Investor”: This is a key strength. If you want to start building wealth but are intimidated by complex brokers, Yuh is ideal. The ability to automatically invest in ETFs with 0% purchase commissions using a savings plan is a powerful and extremely low-cost feature

- The “All-in-One” Seeker: Anyone who values maximum simplicity and wants to combine that free daily account with easy investing (like the 0-commission ETF plans ) and a single, low-cost Pillar 3a.

- Families: It is a standout choice for parents looking to open a free, powerful first account for their teenagers. The “Yuh 14+” account, with its 0% foreign exchange fees, is a huge perk.

Yuh is less indicated for…

- Serious Crypto Users: The “walled garden” (no deposits/withdrawals) and high 1.0% fee make it unsuitable for anyone who wants to truly own their crypto or trade frequently.

- Heavy International Travelers: The 0.95% currency exchange fee on the standard account will add up. Specialized apps like Revolut or Wise are far cheaper for this use case.

- Advanced Tax Planners: If your main goal is to optimize your pension withdrawal, you’ll need a provider like VIAC that allows multiple 3a “pots”.

- Cash-Based Users: If you frequently handle cash (e.g., for work tips or sales), the complete lack of a cash deposit option is a major drawback.

Ready to try Yuh?

Download the app and use our referral code f39tn7 during the sign-up process.

By depositing an initial 500 CHF, you will receive a welcome bonus of 250 Swissqoin to get you started.

Download the app here